Banking on Resilience: A Guide to Disaster Recovery Plans

July 15, 2025

Master it lifecycle management software with lifecycle tracking, automation, and secure retirement for hybrid IT environments.

July 17, 2026

Discover how an it support center delivers expert technical troubleshooting, security, and strategic value for your business.

July 9, 2026

Discover the top software as a service companies shaping 2026 with AI, security, and scalable cloud solutions for your business.

July 7, 2026

July 15, 2025

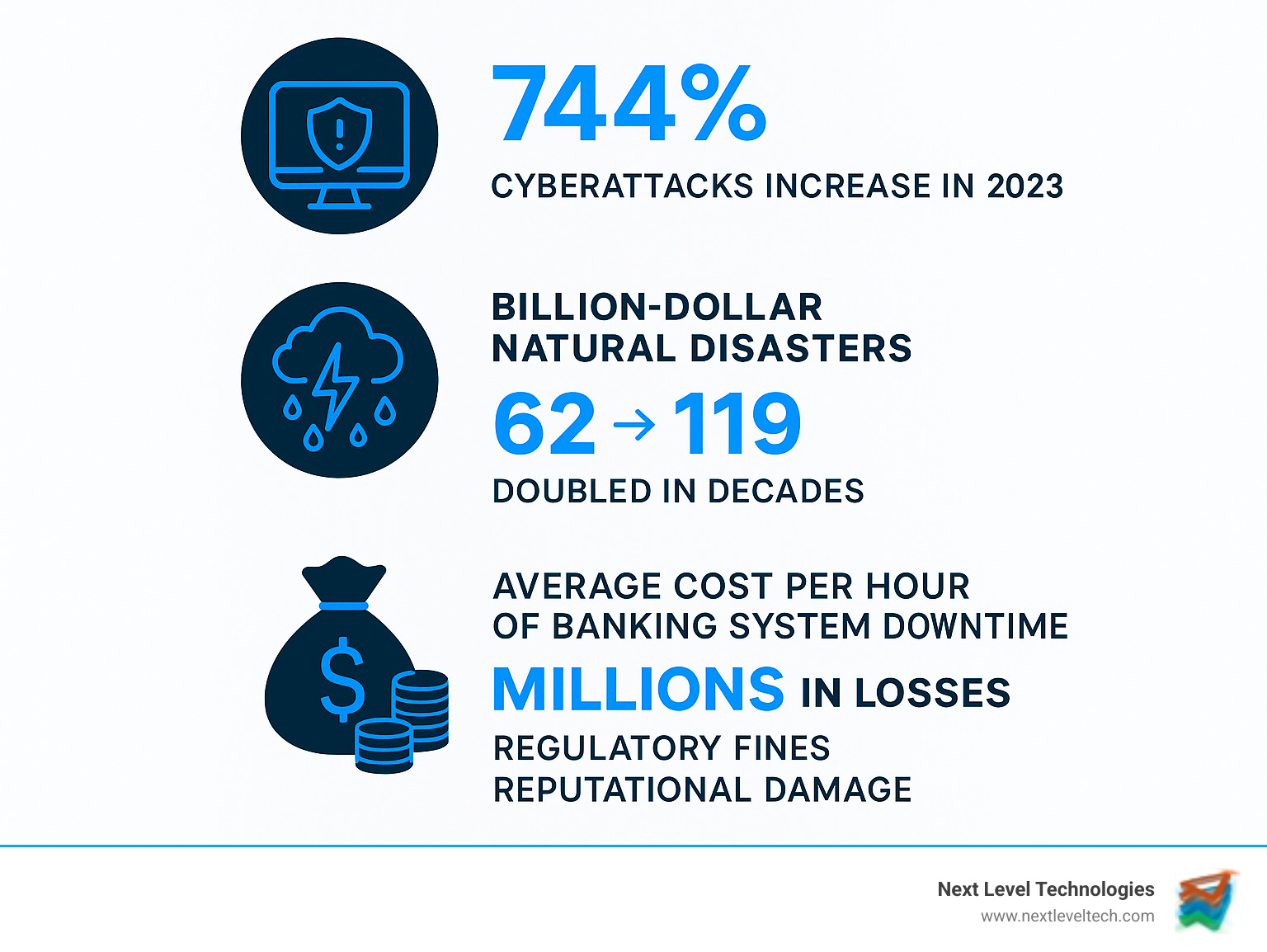

A disaster recovery plan for banks is a concise, documented playbook that enables financial institutions to bring critical IT systems back online after cyber-attacks, natural disasters, or hardware failures. It is the technical foundation of operational resilience. Without a working DRP, a single outage can snowball into regulatory fines, reputational damage, and permanent customer loss.

Key components every bank should document in detail:

Why act now?

With more than 15 years of managed IT and cybersecurity experience in Columbus, OH and Charleston, WV, the Next Level Technologies team has built and tested DRPs that keep Midwest and Appalachian institutions running when others go dark.

Helpful deep-dives:

A Business Continuity Plan (BCP) keeps the entire bank operating; a Disaster Recovery Plan (DRP) focuses strictly on restoring the technology that powers those operations. Think of the DRP as a critical, technical subset of the broader BCP. While the BCP addresses how staff will work from an alternate location or how customer service will function without a branch, the DRP ensures the servers, networks, and data they need are available.

| Aspect | DRP | BCP |

|---|---|---|

| Goal | Restore IT & data | Keep business services running |

| Scope | Infrastructure, apps, backups | People, facilities, vendors, IT |

| Metrics | RTO / RPO | Maximum Tolerable Downtime |

| Triggers | System failure, data loss | Any severe business disruption |

Learn more: IT Security For Banks

Read: How To Protect Your Data From Ransomware

Creating a strong, regulator-ready disaster recovery plan for banks takes four streamlined steps. This process should be a collaborative effort involving IT, operations, risk management, and senior leadership.

The BIA is the cornerstone of your DRP. The goal is to identify and rank all business processes and the IT systems that support them. This involves interviewing department heads to understand their workflows and dependencies. You must determine the operational and financial impacts of a disruption to each service (ACH, wires, core processing, online banking, ATMs, etc.). The analysis should put a dollar value on every hour of downtime, which provides a clear justification for DRP investments. See: IT Disaster Recovery Planning.

With the BIA complete, you can set realistic recovery objectives for each system. This means defining the Recovery Time Objective (RTO) and Recovery Point Objective (RPO). It's common to use a tiered approach. Tier 1 applications, like the core banking platform, might have an RTO of minutes and an RPO near zero. Tier 2 applications, like loan origination software, might have an RTO of a few hours. Tier 3 systems, such as development environments, could have an RTO of 24 hours or more. These objectives must balance business requirements with the budget for recovery technologies.

This step involves creating the formal DRP document. It must be detailed enough for someone to execute it under pressure without prior knowledge. Key contents include:

Your technology choices must align with your RTOs and RPOs. A hybrid approach combining on-premise and cloud solutions often provides the best mix of speed, cost-effectiveness, and geographic redundancy. Key technologies include:

For financial institutions, a DRP is not just good practice—it's a regulatory mandate. Examiners will scrutinize your plan, your testing records, and your board's involvement.

Stay ahead with our IT Compliance services.

Modern banks rely heavily on third parties for core processing, cloud hosting, and specialized fintech APIs. Your DRP is incomplete if it doesn't account for vendor risk. Your vendor management program must include:

A DRP that sits on a shelf is useless. Routine testing and diligent maintenance are what convert a theoretical document into true institutional resiliency. This is a continuous cycle, not a one-off project.

Testing should progress from simple to complex to validate every aspect of the plan. The goal is to find weaknesses in a controlled setting, not during a real crisis.

Critical test scenarios to practice include a ransomware outbreak, a multi-day regional power outage, the total loss of a primary data center, and the sudden failure of a key third-party vendor. More ideas: Business Continuity IT Solutions.

Ignoring DRP is a high-stakes gamble. In the short term, an outage leads to huge financial losses from stalled operations. This is quickly followed by severe regulatory penalties and fines for non-compliance. In the long term, the reputational damage can lead to customer defections and lawsuits, sometimes causing permanent harm to the institution's viability.

DRP ownership is a cross-functional responsibility. While IT typically leads the technical implementation, the plan must be owned by the business. A dedicated DRP coordinator or lead should manage a team that includes senior leadership, IT, risk/compliance, operations, HR, and communications. This ensures the plan aligns with business needs and everyone understands their role.

Operational resilience is a broader concept that describes a bank's ability to prevent, adapt to, and recover from disruptions. The DRP is the technical engine of resilience. It provides the concrete, actionable steps and technological capabilities that allow the broader Business Continuity Plan (BCP) to succeed, ensuring the bank can absorb shocks and continue serving its customers and the financial system.

The cloud introduces both opportunities and new considerations. It can make DR more affordable and flexible through services like DRaaS. However, it also introduces a shared responsibility model. Your bank is still responsible for its data and for having a plan. You must understand your cloud provider's DR capabilities and SLAs and integrate them into your own plan. You cannot simply outsource the responsibility.

The very first step is to follow the plan. This typically means the designated authority officially declares a disaster, which triggers the activation of the recovery team. The team then assembles (physically or virtually) and immediately begins executing the pre-defined communication plan to notify key stakeholders while the technical team starts the recovery procedures.

A robust, tested, and consistently updated disaster recovery plan for banks is no longer just a compliance checkbox; it is a fundamental pillar of modern banking and a significant competitive advantage. The ability to withstand disruption is a direct measure of an institution's stability and its commitment to protecting customer assets and trust. From the regulatory pressures of the FFIEC to the ever-present threats of cyber-attacks and natural disasters, the need for a proven recovery strategy has never been greater.

When floods hit Charleston or a sophisticated cyber-attack rolls through Columbus, institutions partnered with Next Level Technologies have the confidence to continue processing transactions while others scramble. A resilient DRP ensures continuity, protects the brand, and reinforces customer loyalty.

Leverage our 15+ years of managed IT and deep cybersecurity training to build, test, and maintain a DRP that protects your customers, your reputation, and your bottom line.

Ready to harden your bank’s resilience? Partner with us for expert managed IT services and support.

Master it lifecycle management software with lifecycle tracking, automation, and secure retirement for hybrid IT environments.

July 17, 2026

Discover how an it support center delivers expert technical troubleshooting, security, and strategic value for your business.

July 9, 2026